|

|

|

|

|

|

https://gothamist.com/news/future-of-nycs-iconic-yellow-cabs-looks-like-another-ride-hailing-app

New York City’s yellow cabs may operate and function more like their ride-hailing app competitors in the future, according to the Taxi and Limousine Commission’s strategic plan released late Friday.

The agency said it wants to roll out shared rides, variable pricing and be included in transit apps that compare taxi prices to other ride services “in the coming years.”

“TLC is excited about ways that technology and innovation can facilitate the taxi industry’s continued recovery from the impacts of the pandemic,” TLC Acting Commissioner Ryan Wanttaja wrote in a statement. “The Taxi Strategic Plan includes big ideas that will help ensure the long-term viability of the industry, and we are looking forward to working with drivers, industry members, and other stakeholders on implementing these initiatives.”

The plan includes 40 recommendations, some of which are currently underway, like the medallion debt relief program. Other ideas would change the way yellow cabs have historically operated, with plans to open the door to testing automated vehicles and exploring a future of prices that rise and fall based on demand, as opposed to a flat meter rate.

The TLC said it is committed to “supporting the Taxi industry and its future as a critical part of New York City’s transportation network,” and noted these 40 suggestions were created as “a first step to ensuring the continued viability of the industry.”

The yellow cab industry has been facing headwinds for a decade now. For-hire vehicle apps entered the city in 2012, leading to a decline in taxis.

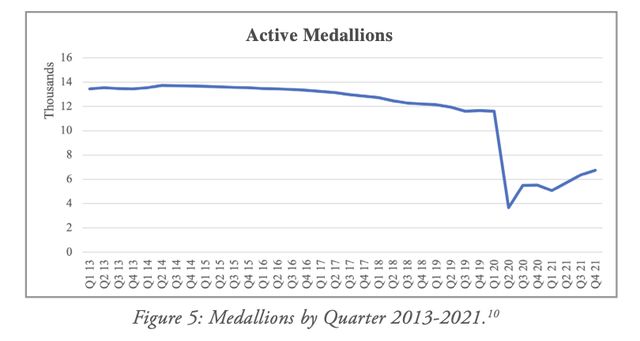

The value of a taxi medallion was more than $1.2 million in 2014, but is now worth about $100,000. The medallions’ nosediving worth has sent owners – taxi drivers who thought the medallion was a foothold in the middle class – into financial and mental crises.

These upheavals have been further exacerbated by the pandemic, which has wiped out any fares from tourism and business sectors. The TLC’s initiatives received mixed reactions, with the drivers’ union hoping for more actions to improve workers’ livelihoods and drivers eager for any possible changes that will earn them higher wages.

Bhairavi Desai, executive director of New York Taxi Workers Alliance which represents taxi drivers, said she was glad to see that the TLC plan includes increasing the flat rates to and from the airports, as well as continuing with the medallion debt relief.

The medallion debt program, which was announced last November , followed a two-week hunger strike workers went on last year, seeking relief from the city. The strategic plan notes that the city has agreed to be the guarantor on the principle of medallion loans that are written down to “$170,000 or less, with an interest rate of 5% or less, and that are fully amortized over 20 years.”

But Desai said she was dismayed that the TLC is trying to change the way yellow cabs operate to make them function more like Uber and Lyft.

“We need to replace that economic model that’s already left Uber and Lyft drivers at sub-minimum wages and use this as an opportunity to elevate the standard so all drivers can earn more,” Desai said.

But some yellow cab drivers said they think the TLC’s plan is a positive move.

“We need something to compete with Uber, and I think this is the right step. I feel like this should help the yellow cab industry,” Al Khan said. “I’m hopeful … I don’t see the downside.”

Khan, a 29-year-old Staten Island resident, has been driving for 10 years. He said he would still like to see the city restrict more for-hire vehicles from being allowed on the streets.

The TLC’s document noted it will continue to reevaluate the number of for-hire vehicles every six months and will decide whether to issue new licenses.

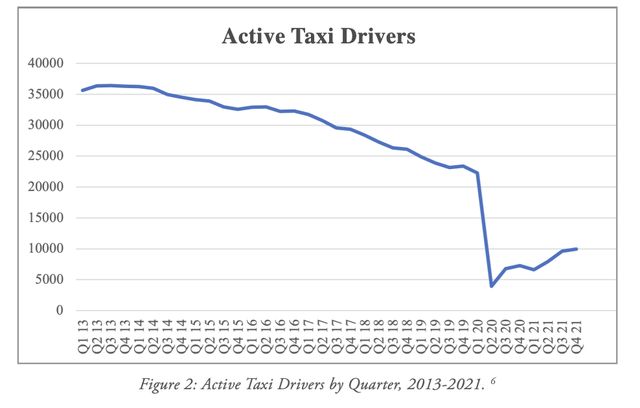

While there are 13,587 taxi medallions, the document notes at the end of 2021, only 6,750 were actively picking up passengers, while the others were in storage.

Yellow cab ridership is still down from pre-pandemic levels. While there were over 250,000 taxi rides in February 2020, there were about 106,000 this February. Still, that’s an increase from January 2022, which saw just 79,000 taxi trips.

The TLC plan also calls for advocating to avoid any additional MTA congestion pricing charges. The first phase of congestion pricing, which passed the state legislature in 2019, included a $2.50 surcharge on all taxis that drive below 96th Street, which the TLC document notes is nearly every trip that isn’t an airport trip. The details of the next phase, how much drivers that enter the congestion zone below 60th Street might be charged and which vehicles would be exempted, will likely be announced later this year.

“TLC will work with industry stakeholders and governmental partners to advocate that Taxis be excluded from congestion pricing,” the plan noted.

The MTA hasn’t said if taxis will be exempt from the higher charges, which could be as much as $23 for an E-Z pass user, and $35 for others, according to details during the first round of public hearings on congestion pricing.

“Any credits, discounts or exemptions for any vehicles need to be counterbalanced by not just charges on other drivers, but also on the impact they will have on traffic flows as the primary purpose of the Central Business District Tolling Program is to reduce congestion in the central business district and raise sufficient funds to support $15 billion for the region’s subways, buses and commuter railroads,” MTA spokesperson Aaron Donovan wrote in a statement.

Still, other drivers said there are things the TLC can’t control that are still contributing to low wages and ongoing hardships for drivers, like gas prices, and the cost of leasing vehicles

“We are suffering,” MD Islam, 52, who has been driving a cab for eight years, said. “Lose money, too much lose money, that’s the problem.”

(Reuters) - Bankruptcy filings have started to increase this year and the number of new cases filed in March jumped significantly from February, but remain below last year's numbers, according to data released on Tuesday by legal research firm Epiq.

The total number of new commercial and consumer bankruptcies filed in March grew 33.5% over the month prior, according to Epiq, with consumer filings increasing by 34% and commercial cases jumping by 26%. Those figures build on the slight upward trend that began in February, which brought 3% more new bankruptcies than January, according to Epiq’s data.

But, the overall number of filings are still down compared to last year. The first quarter of 2022 brought a 17% decline in new filings compared with the same period in 2021, with consumer cases down 16% and commercial cases down 25%.

Bankruptcy filings have largely dipped since the COVID-19 pandemic hit the U.S. in March 2020, as government aid programs helped keep individuals and businesses afloat. But experts say that as those aid packages dry up, people and companies alike will start seeking debt relief via bankruptcy again.

“Amid rising interest rates, growing inflation concerns, worker shortages and supply chain challenges, access to bankruptcy is imperative for struggling consumers and businesses,” Amy Quackenboss, executive director of the American Bankruptcy Institute, said in a statement on Tuesday.

Chapter 11 cases, which encompass larger commercial bankruptcies, were up 38% in March over February, but down 43% for the first quarter of 2022 compared with the same period in 2021.

Small business bankruptcy filings known as subchapter V cases, a new type of filing that went into effect in February 2020 under the Small Business Reorganization Act, hit record numbers last month. Epiq said the 81 cases filed the week of Mar. 21 is the highest weekly total ever for that type of bankruptcy.

That spike came just before the $7.5 million debt limit for businesses that file under subchapter V was set to drop down to $2.7 million, though legislation is underway to permanently bring the debt limit back up to $7.5 million.

Individual filings could also increase if Congress passes legislation that would increase the debt limit under Chapter 13 of the bankruptcy code to $2.75 million from the existing $1.2 million. The bill, which was introduced in the Senate last month and has bipartisan support, aims to simplify eligibility for Chapter 13 protection and make it easier for self-employed people to qualify for bankruptcy relief.

Preoccupied Congress Fails to Act, Sending Debt Limit Back Down to $2.7 Million and Reducing Availability of Subchapter V Protection for Small Businesses See article at https://lnkd.in/dMyGQWq6

https://www.nytimes.com/2022/03/28/technology/uber-taxis-san-francisco-deal.html

Interesting article about Boris Becker bankruptcy filing and allegedly hiding assets. The article can be found at https://www.espn.co.uk/tennis/story/_/id/33570612/boris-becker-acted-dishonestly-hiding-wimbledon-australian-open-trophies-declaring-bankruptcy?platform=amp

Jim Shenwick, Esq 212 541 6224 jshenwick@gmail.com

https://www.crainsnewyork.com/politics/chuck-schumer-and-new-york-elected-officials-blast-taxi-medallion-lender

Readers of our posts are aware that at Shenwick & Associates we do personal and business bankruptcy filings and workouts for many clients.

In addition, we review settlement agreements for clients so that the settlement payments are not captured by section 547 of the Bankruptcy Code as a preference (also known as "preference proofing a settlement agreement"). This week we were retained by 2 clients who wanted their settlement agreements reviewed regarding preference exposure.

This work is usually referred to us by the client or the client's litigator.

There are generally 3 signs that indicate that a defendant may file for bankruptcy protection either after the settlement agreement is signed or after making some or all of the payments required by the settlement agreement.

During settlement negotiations, the defendant discusses filing for bankruptcy.

During settlement negotiations, the defendant discusses closing its business or

The defendant asks for more than 30 days to make the initial settlement payment.

In the event that a defendant files for chapter 7 bankruptcy within 90 days of making a payment to the plaintiff, that payment may be a voidable preference and subject to recapture or clawback by a bankruptcy trustee in a chapter 7 bankruptcy proceeding.

Clients will be extremely upset and point fingers if their settlement payments are clawed back by a bankruptcy trustee or they need to defend a lawsuit (adversary proceeding) by a bankruptcy trustee seeking to recapture those payments.

What can be done to preference proof a settlement payment?

Below are some suggestions and strategies, but a risk will always remain until 90 days have passed from the date of payment.

Seek financial statements from the defendant or better yet a financial statement under penalty of perjury (an Affidavit of Net Worth), Have your CPA or a bankruptcy attorney review those financial statements.

Seek a guarantee of the payments from a 3rd party.

Make the plaintiff a secured creditor by receiving a mortgage on real estate or a security agreement and ucc-3 on another asset like accounts receivable.

Structure the settlement agreement so payments are made sooner rather than later.

Have the defendant stipulate to a judgment or a confession of judgment and have the plaintiff provide a satisfaction, 90 days after payment is made.

Delay providing a release to the defendant until 90 days have passed from payment.

Use the “earmarking doctrine” which provides that payments that are supplied by a 3rd party such as a bank or a malpractice insurer and earmarked for payment to a creditor are not preferential.

Language should be included in the settlement agreement that preserves the plaintiff’s claim if any settlement payments are recaptured.

Finally the settlement agreement should state that if the defendant files for bankruptcy the automatic stay, provided for in section 362 of the bankruptcy code is deemed lifted with respect to the Plaintiff.

Although no single factor may win the day, a plaintiff should attempt to obtain as many of the above points as possible.

Plaintiffs or their counsel having questions about settlement agreements and preferences should contact Jim Shenwick, Esq. 212-541-6224 or jshenwick@gmail.com

CBS News (link below) has an article about impact of Omicron virus on restaurants. https://www.cbsnews.com/amp/news/restaurants-closing-2022-without-aid-restaurant-revitalization-fund/#app

At Shenwick & Associates we have been working with many restaurants whose business has been impacted by Omicron and the guarantors of those leases. Jim Shenwick 212 541 6224 jshenwick@gmail.com

Harold Israel, Esq. at Levenfeld Pearlstein, LLC is reporting that the Sub V Bankruptcy Debt limits, which had been temporarily increased to $7,500,000.00, are posed to be made permanent.

Interesting article in newsy.com (URL below) about how the Biden Administration is addressing student loan debt. https://www.newsy.com/stories/president-biden-s-policy-on-student-loan-debt-cancellation/

As many readers are aware, individuals whose income exceeds the median income in New York State are required to do "means testing" to determine if they qualify for chapter 7 personal bankruptcy.

In New York State the median income for a family of 1, 2 or 3 is listed below and if a Debtor’s income exceeds the state’s median income they must do means testing.

Household Size Monthly Income Annual Income

1 $5,058.00 $60,696.00

2 $6,429.92 $77,159.00

3 $7,709.00 $92,508.00

If an individual wants to file for chapter 7 bankruptcy and they do not pass the means test, then there is a "presumption of abuse" and they are not allowed to file for chapter 7 bankruptcy.

The means test is an 8-page test and it is the most complicated test or calculation in the law!

Shenwick & Associates is often referred complex bankruptcy cases and we do means testing on a regular basis.

We are often asked whether non-dischargeable student loan payments are an allowed deduction for means-testing. Interestingly, the test itself does not allow a deduct for non dischargeable student loan payments. However there is a deduction for " special circumstances" and many bankruptcy attorneys believe that non-deductible student loan payments should be a special circumstance deduction.

There is a case on point from the Western District of New York (it is not a case from the Southern or Eastern Districts), but it holds that non-deductible student loan debt can be deducted when doing means testing and the logic of that case may be persuasive to judges in this District. The name of that case is in re Howell 477 B.R. 314 (2012).

In the Howell case, the United States Trustee has moved to dismiss this Chapter 7 case on grounds that the granting of a bankruptcy discharge would constitute an abuse. The central issue in the case was whether the obligation to pay a non-dischargeable student loan can serve as a special circumstance that will overcome a statutory presumption of abuse under 11 U.S.C. § 707(b)(2).

Section 707(b)(1) of the Bankruptcy Code establishes the general rule, that the Court may dismiss a case filed by an individual debtor under this chapter whose debts are primarily consumer debts if the filing would be an abuse.

In the Howell case, the debtor had student loan payments of $658.00 per month and if this deduction were treated as an allowable expense, their current monthly income would fall to a level that avoids a presumption of abuse.

Section 707(b)(2)(B)(i) of the Bankruptcy Code states that in any proceeding to dismiss a case for abuse, "the presumption of abuse may only be rebutted by demonstrating special circumstances.

The Court found that there was no evidence that the Debtors lead an extravagant lifestyle.

The Debtors had three outstanding student loans. In sworn affidavits, the Debtors stated that they were not eligible for any further extensions and that as presently constituted, the loans require monthly payments through dates that range between 16 and 24 years after the filing of their bankruptcy petition.

The Judge held that the totality of evidence supports the absence of an abusive filing and that Section 707(b)(2)(B)(i) provides that special circumstances" may rebut the presumption of abuse.

The Court stated that the non-dischargeable character of the debtors' student loans will necessitate expenses for which the debtors have no reasonable alternative.

The Judge further found that the magnitude of the student loans will further compel substantial payments over an extended period of time, without hope for any deferral.

The Judge held that based on the debtor’s student loans and non extravagant lifestyle the bankruptcy filing was non-abusive and the Debtor’s were granted their chapter 7 discharge.

We should note that the debtors were not attempting to discharge their student loans in their chapter 7 bankruptcy filing.

Individuals that have questions about Personal Bankruptcy or the Means Test should contact Jim Shenwick 212 541 6224 or jshenwick@gmail.com

https://www.reuters.com/world/us/upside-down-again-omicron-surge-roils-us-small-businesses-2022-01-16/

Bankruptcy Deadlines must be observed! The recent case of In re U-Haul, 21-bk-20140, 2021 Bkr LEXIS 3373 (Bankr. S.D. W. Va. Dec. 10, 2021) demonstrates this rule. In the U-Haul case, a creditor needed to file a proof of claim for $53 million and their attorney waited until the last moment to do the filing. Unfortunately the attorney did not have the proper password and the proof of claim was filed approximately 9 hours late.

Counsel for the Debtor objected to the late filed claim. Creditor counsel argued “excusable neglect” (the argument usually made by attorneys when deadlines are missed see Pioneer Inv. Servs. v. Brunswick Assocs. Ltd P’ship, 507 U.S. 380 (1993)) and creditor counsel lost.

For those that do bankruptcy work on a day to day basis, this is a painful case to read.

A lesson for all lawyers is to prepare for deadlines, observe deadlines, do not wait until the last minute to file and prepare and plan for the unexpected. Jim Shenwick, Esq.

https://www.forbes.com/sites/zackfriedman/2022/01/04/is-student-debt-cancellation-next/

Due to a lack of action by Congress, the Small Business Bankruptcy Law known as Sub V, debt limit, will be reduced to $2.7 million, which will limit the number of distressed companies that will be able to file for Sub V bankruptcy protection. Jim Shenwick 212 541 6224 jshenwick@gmail.com